Consumers reported spending 8% less on technology in the month of October according to IDC’s October Purchase & Subscription Index survey, which measures consumer expenditures on devices and tech-enabled services. In addition, consumers plan to spend less on tech gifts this year-end. Learn what you can do to drive sales and be successful in this environment.

Spend Falls to July Level, Raising Year-End Concern

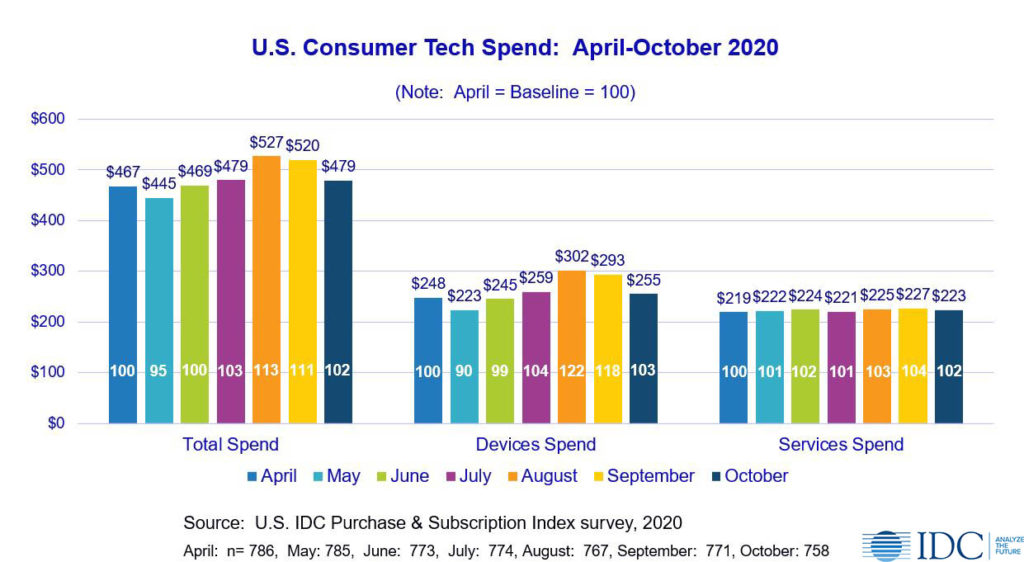

After extremely strong spending in August and September, consumers’ spending in October returned to the July level, just 3% ahead of our April baseline. This naturally prompts a level of concern as the year-end holiday season ramps up.

Questions immediately come to mind. “Now what? Does this mean consumer spend is going to fall off a cliff? Is this a natural lull before the acceleration of year-end spending or is this a more significant pullback in consumer spend?”

Big Drop at the Top of the Market

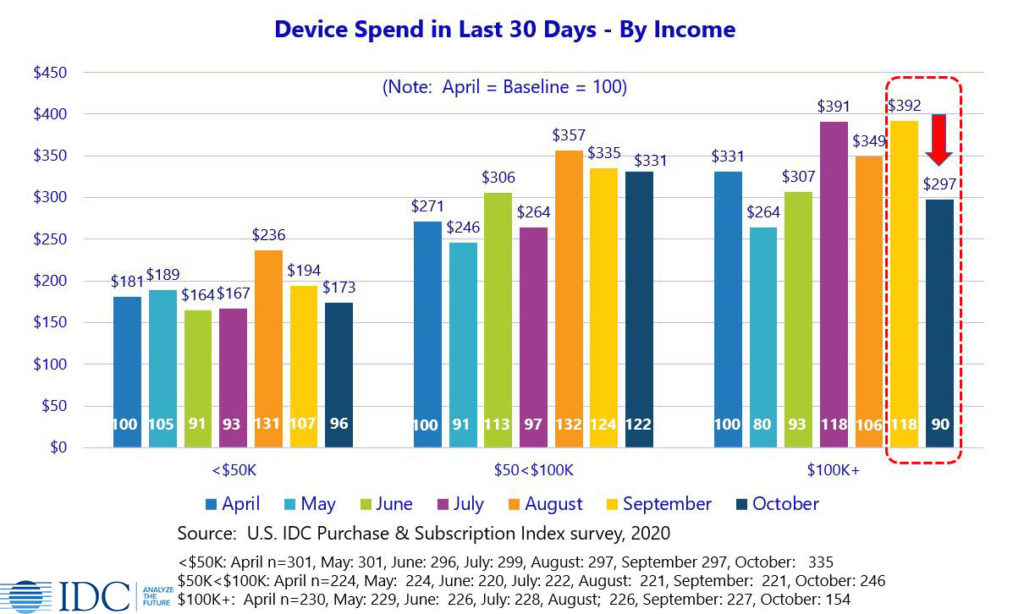

This large downward movement was driven by a precipitous drop in device spend among those with incomes of $100,000 or more. Device spend among those with incomes under $50,000 also dropped. But that was anticipated given the trajectory in their spend and the attitudes they had expressed. However, those with high incomes had been bullish – both in attitude and behavior – so this big drop is a surprise.

Drilling Down on Higher-Income Buyers

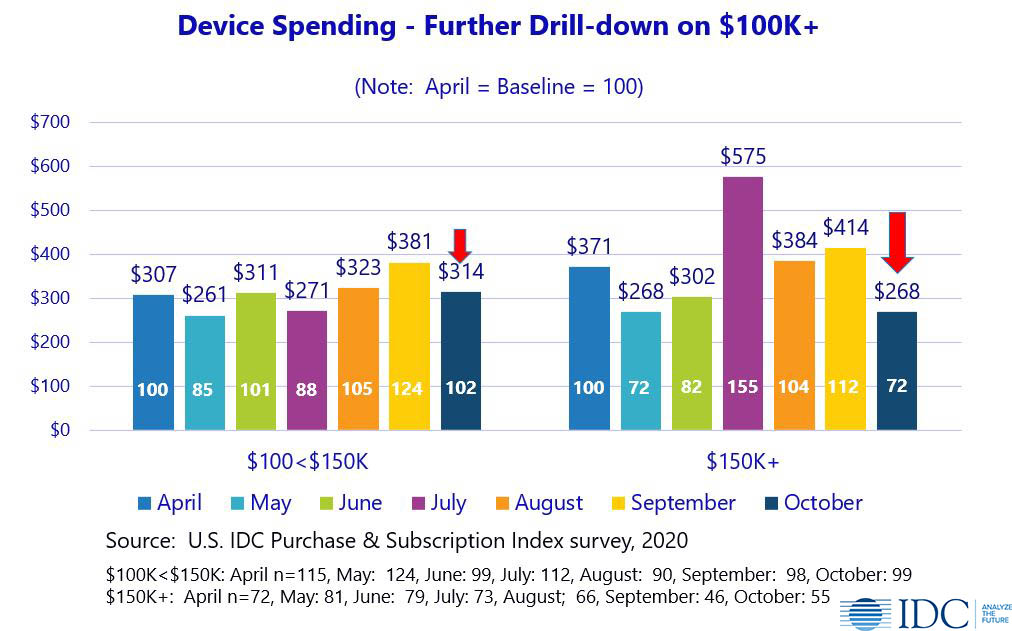

Examining the data more closely, we can see that device spend dropped more dramatically among those with incomes above $150,000. Their spend fell below that of those with incomes between $100,000 and $150,000, returning to its May level.

The expenditures of these high-income ($150,000+) households are more discretionary – want-driven rather than need-driven – making them easier to postpone or even cancel entirely. We can see this in their attitudes – very different from what we observe with those in the $100,000 to $150,000 income bracket where their sense of need and motivation to purchase is intensifying.

Importantly, both groups remain optimistic about their spend over the next 30 days. At the same time, there are other considerations. Despite their optimism, the $100,000-$150,000 group increasingly feels it is spending too much on tech. The $150,000 group is fickle; this is not the first time this year that we have seen this group fail to spend as much as expected. Whether concerns about the election or other factors are at play, we cannot be sure.

Consumers Plan to Spend Less on Gifts this Year-End, Including Tech

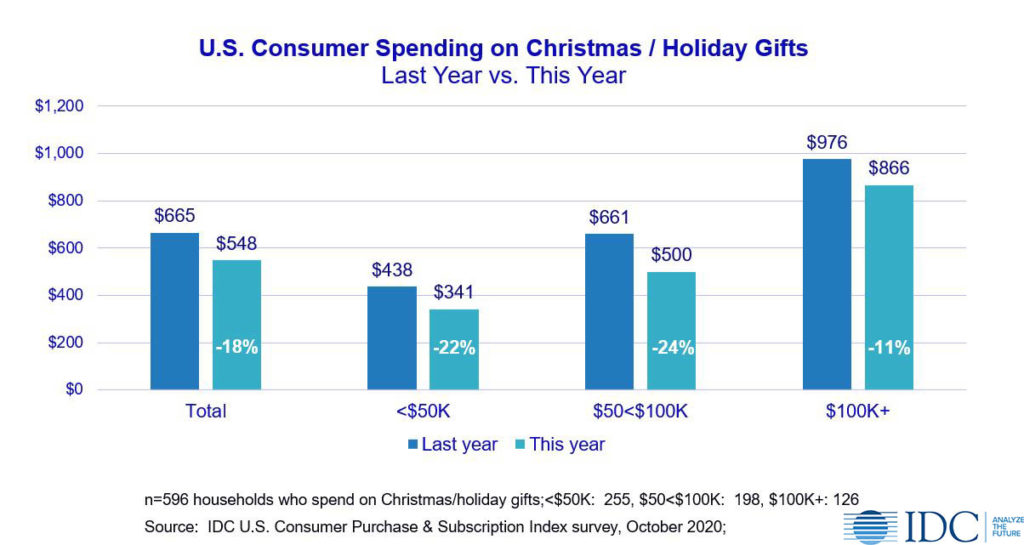

When asked directly about their Christmas and holiday spending plans, consumers say they will spend just under $550 this year. That’s down 18% from the amount ($665) they reported spending last year. Those with incomes under $100,000 plan an average cutback of 23%. Higher-income households will also cut back but only half as much (11%).

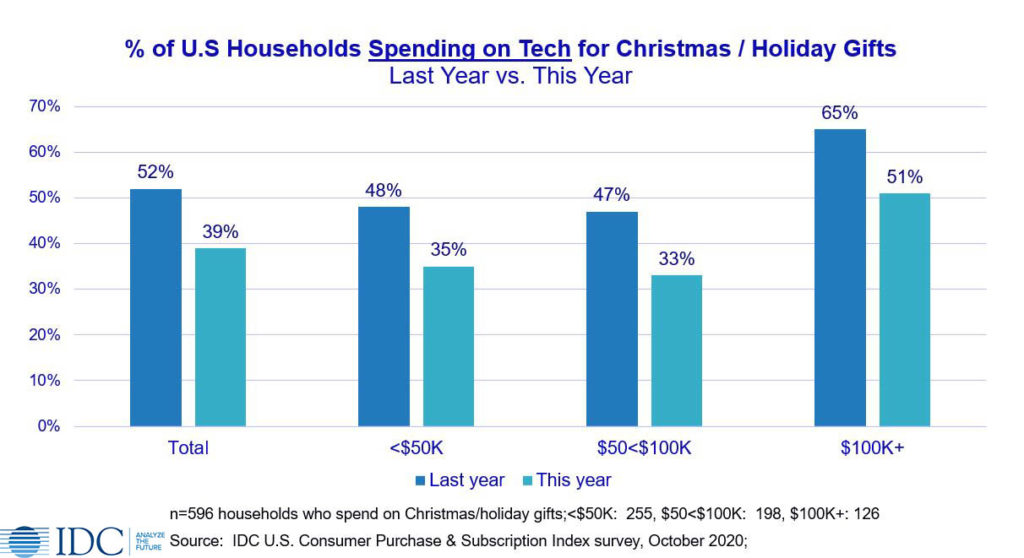

Not only do consumers plan to spend less overall on their Christmas/holiday gifts, a smaller percentage plan to spend on tech for gifts this year. A little over half (52%) of households report spending on tech last year, while only 39% plan to do the same this year. Among those with incomes under $100,000, only 1 in 3 plan to spend on tech, while half of higher-income buyers still plan to spend on tech.

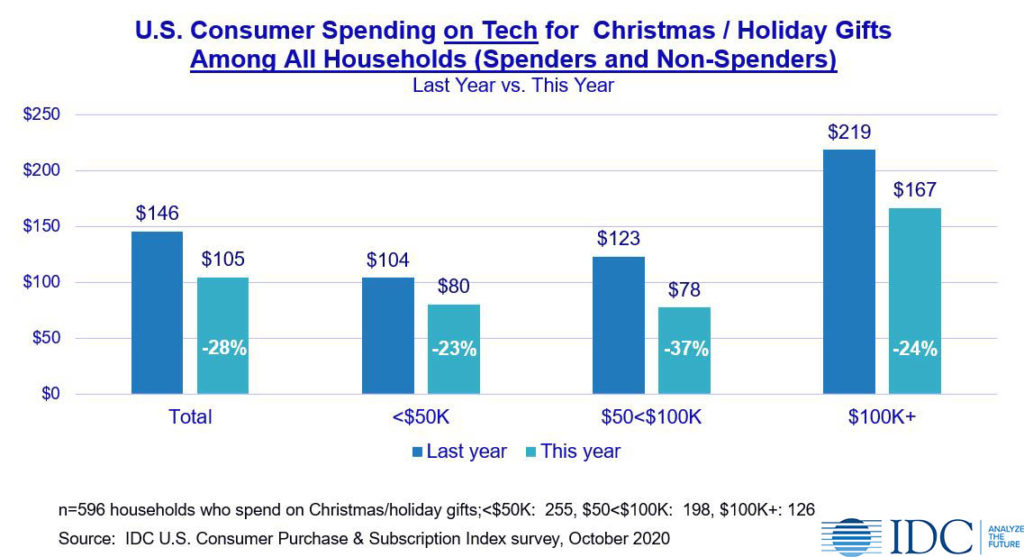

If what consumers say about their Christmas and holiday spending plans were to cometo fruition, total tech spend on Christmas gifts (among spenders and non-spenders) would be 28% lower than last year – largely due to the smaller percentage of people spending on tech this year. The biggest percentage reduction would come from middle-income consumers.

Tech Spend per Spending Household to be Down Only Slightly

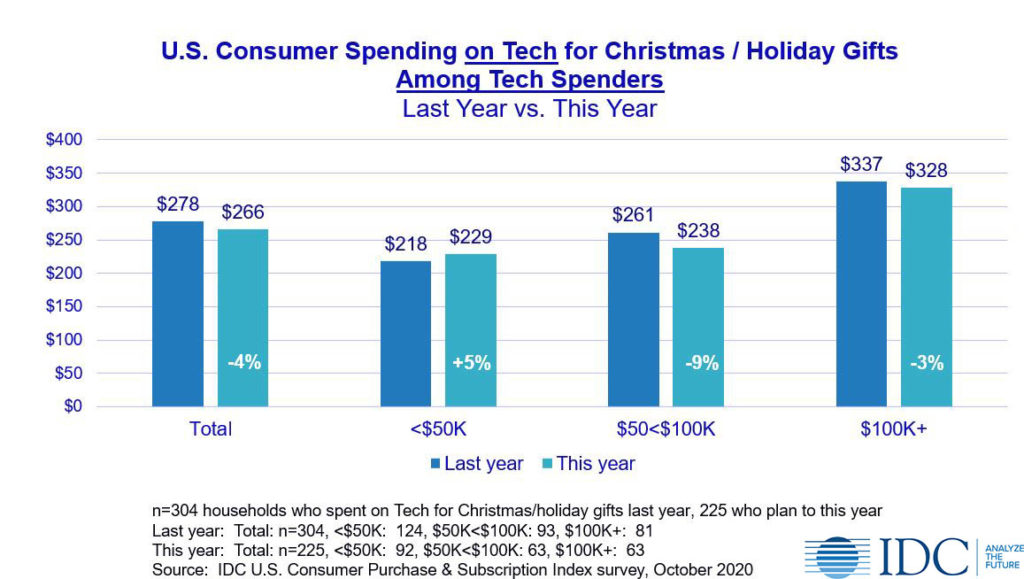

Importantly, among those who plan to spend on tech this holiday season, the planned expenditure per household is quite similar to last year – down only 4% overall. In fact, lower-income buyers plan to spend an average of 5% more than last year. And among higher-income buyers, the planned reduction is minimal.

But Tech Spend Will Take Up a Larger Share of Tech Spenders’ Budget

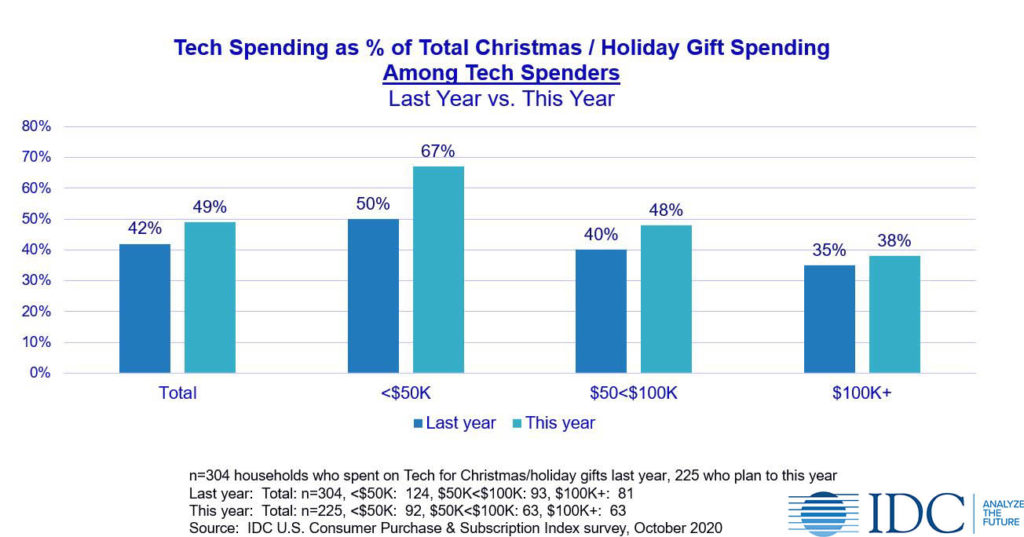

For marketers, it’s important to put this in perspective, so that they understand consumers’ realities. For this year’s tech gift-spenders, their planned spend will amount to nearly half (49%) of their total spend on gifts, compared to 42% last year. More importantly, for those with incomes under $50,000, that amount will go from half of what they spend to 2/3 of what they spend on gifts. This will force consumers to make starker choices.

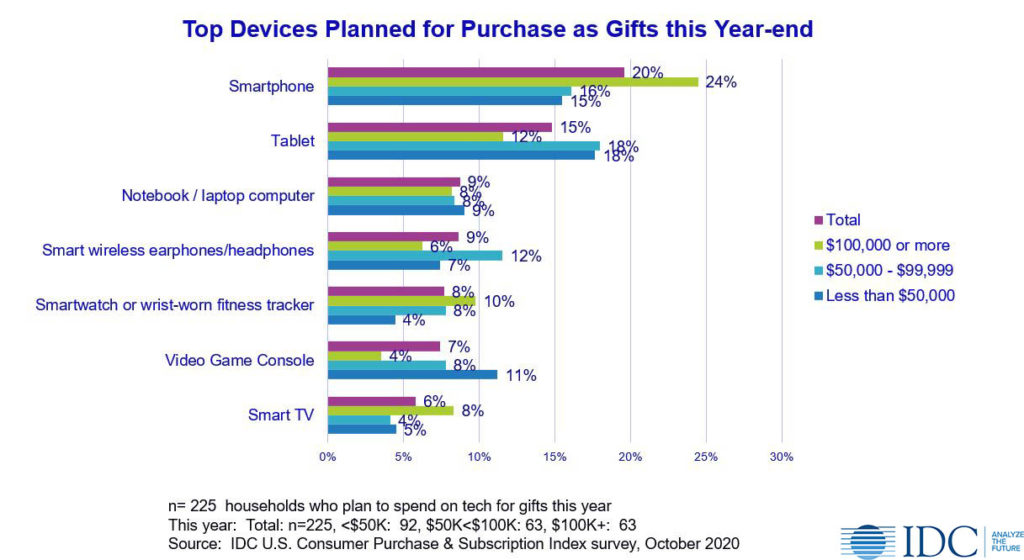

Resonating with Consumers – Top Devices for Purchase

This means it’s more important than ever to know which products consumers want and what will resonate with them. Smartphones and tablets top consumers’ lists across all three income categories. Smartphones, smart watches, and Smart TVs are more important to higher-income buyers. Tablets, video game consoles, and hearables are higher priorities for those in the other two income groups.

Key Takeaways & Actionability for Consumer Marketers

- The big drop in consumer technology spend in October – combined with consumers’ intent to spend less on gifts this year-end – presents a dual challenge for technology marketers and retailers.

- In the simplest of terms, “How to get more consumers to spend at least some of their Christmas/holiday gift budget on tech?”

- “How to do this while battling for a bigger share of a smaller budget?”

- Compelling value propositions are more important than ever.

- In some years, new launch products may sell themselves – not this year.

- Be creative. Well thought out promotions or bundles will drive buzz and catch consumers’ attention in a unique way, prompting word of mouth.

- The role of aggressive price promotions cannot be ignored but should not be the only tactic; avoid a desperate tone.

- Target unplanned (impulse) purchases; this will be crucial to offset the planned drop consumers have in mind.

- Emphasize cool, exciting features and their emotional appeal in advertising, including online and in-store.

- Creatively package small items and accessories of all kinds and position them as stocking stuffers, with tiered pricing:

- Hearables, phone and gaming accessories, streaming sticks, even smart watches and fitness trackers can play this role

- Retailers might even want to consider packaging tech products or accessories with unrelated, non-tech items like chocolate or wine.

- There is opportunity at the top and bottom of the market.

- Those with incomes over $100,000 still present the biggest opportunity.

- Target those with incomes between $100K and $150K, appealing to their aspirations as they are feeling an increasingly intense desire to purchase a range of tech products and services.

- Ensure deals and financing are readily available, given their concern they are spending more than they should on tech.

- Target those with incomes between $100K and $150K, appealing to their aspirations as they are feeling an increasingly intense desire to purchase a range of tech products and services.

- For lower-income consumers, video game consoles and smart wireless earphones are compelling reasons to shop.

- Those with incomes over $100,000 still present the biggest opportunity.

IDC’s Consumer Technology Strategy Service (CTSS) leverages a system of frequent consumer surveys to provide B2C marketers with the full view of the consumer they need to anticipate and meet changing consumer needs and to outperform their competitors. This includes robust monthly data, timely insights, quarterly webinars, and ongoing analyst access.

In addition to my syndicated service, I work closely with clients on custom research projects and consulting. Find out more here.