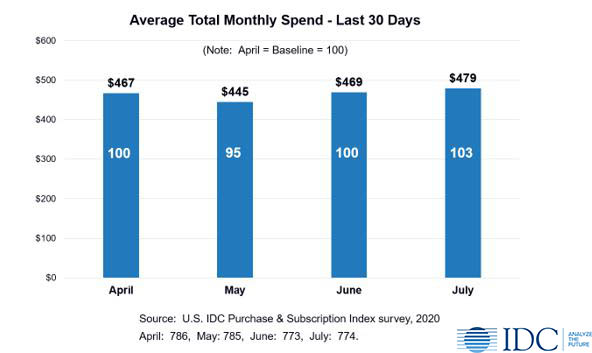

July’s results are in for IDC’s Consumer Purchase & Subscription Index survey. Consumers reported further expanding their tech spending over the last 30 days, surpassing the April baseline for the first time. Let’s take a closer look at the numbers.

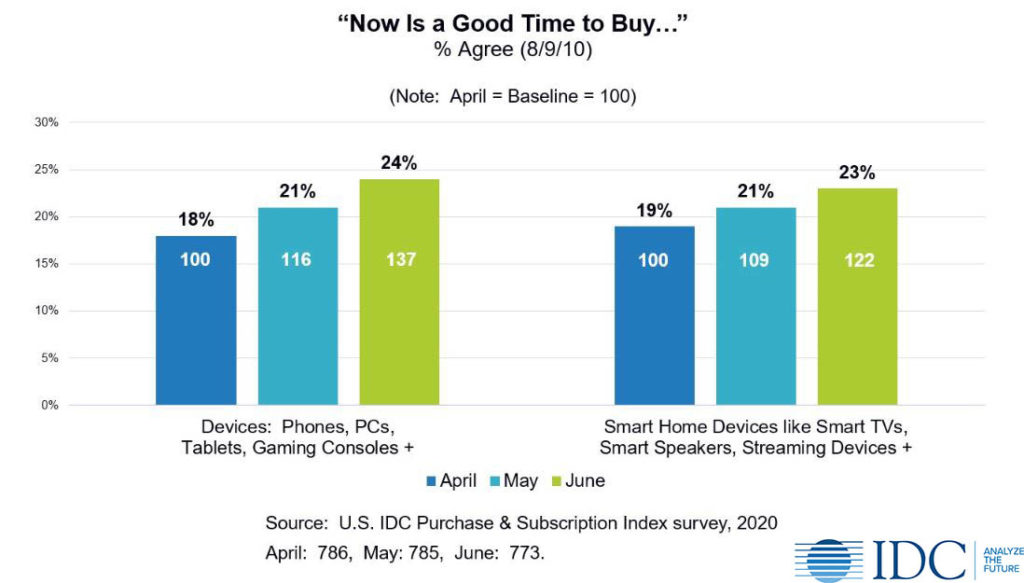

Consumers’ Attitudes in June Clearly Signaled July Expansion

In the June survey results, we saw this increase in July consumer spending coming. Consumers were noticeably bullish about the environment for device spending.

Consumers of all stripes agreed that it was a good time to buy personal devices, gaming devices, and smart home devices.

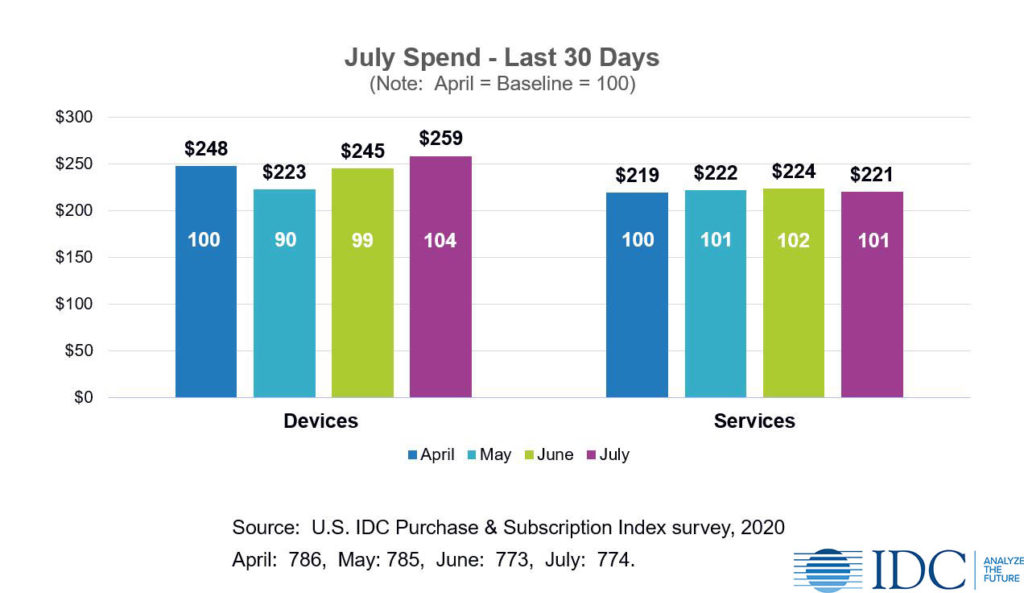

Devices Led the July Expansion

Overall, these attitudes and intentions came to fruition in our July survey results. Device spending drove the July growth in consumer tech spending; consumers reported spending 4% more on devices in July than they did in April.

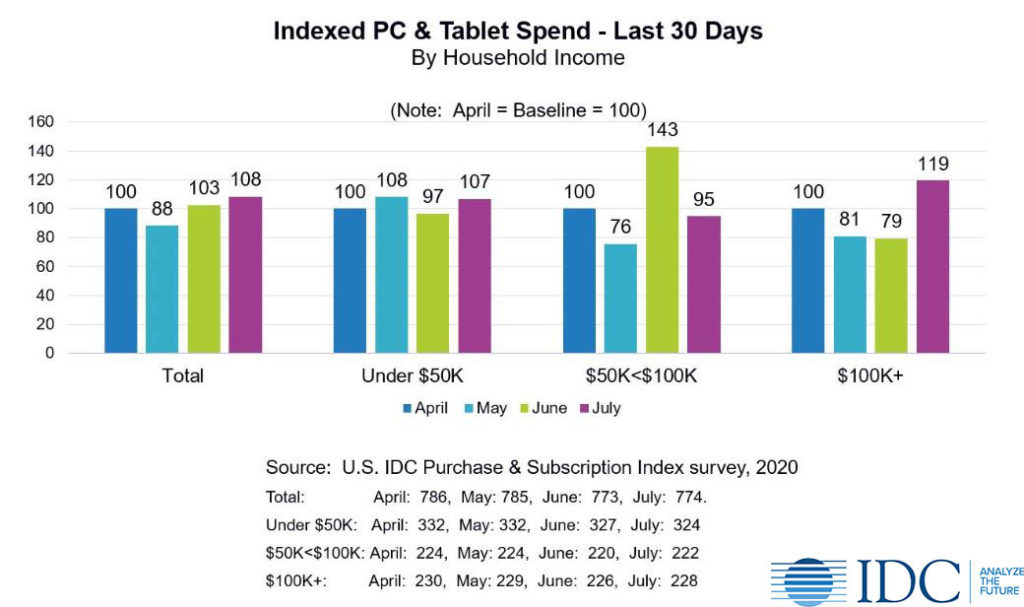

A closer look reveals that households with incomes of $100,000 or more reported a significant increase in their device spending, though not as much as expected. Their July expansion in device spending was relatively timid compared to what they had signaled in June interviewing.

On the other hand, those with incomes under $50,000 surprised us by also spending more on devices. Accustomed to living from paycheck to paycheck, and with some facing the end of supplemental unemployment benefits, these consumers expanded their device expenditures as if concerned about missing out on “their last chance” to take advantage of the opportunity afforded by the current environment.

These increases in spending at the top and bottom of the market offset reductions in spending by those in the middle of the market (those with incomes between $50,000 and $100,000).

Consumers’ self-reported spend on PCs and tablets illustrates this point. Consumers at the top and bottom of the market spent more, while those in the middle-income group pulled back.

There were also some interesting differences between the groups. Those with lower incomes increased their spend on mobile phones and digital media adapters (set-top boxes and streaming sticks). Those with higher incomes increased their spend on a broader range of smart home devices, hearables, and phone accessories.

Disposable Income and Savings Remain at High Levels

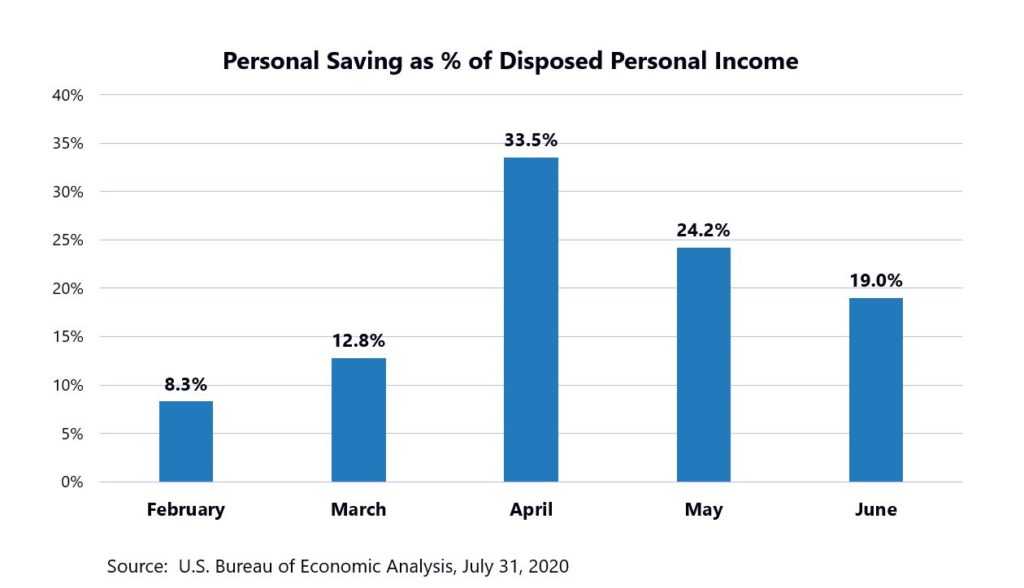

Consumer savings of disposable income remains at extraordinarily high levels (19.0%) according to the Bureau of Economic Analysis, down from its peak in April (33.5%) but more than twice that of February’s pre-COVID level (8.3%).

While consumers have “saved” this money, most of it is not ultimately earmarked for savings. Instead, consumers are likely to wind up spending most of it, since this savings is the result of not making the same level of expenditures on gasoline, restaurants, entertainment, and other expenses as they would in “normal” times.

Indeed, a detailed analysis of consumer expenditures shows tech getting “more than its fair share” of consumer spending. Continued high savings rates signal continued opportunity for the tech industry.

If approved, an additional round of stimulus is likely to provide additional disposable income, even if more focused or less generous than the first round.

Looking Ahead – A Cloudy Picture

Moving forward, the picture is less clear. Consumer sentiment and sense of need show some signs of softening, particularly among those with incomes of less than $100,000.

Those earning $100,000 or more continue to signal a growing sense of need and strong interest in devices. However, they have consistently held back over the last couple of months, spending less than expected. Their “bark” has been “worse than their bite.”

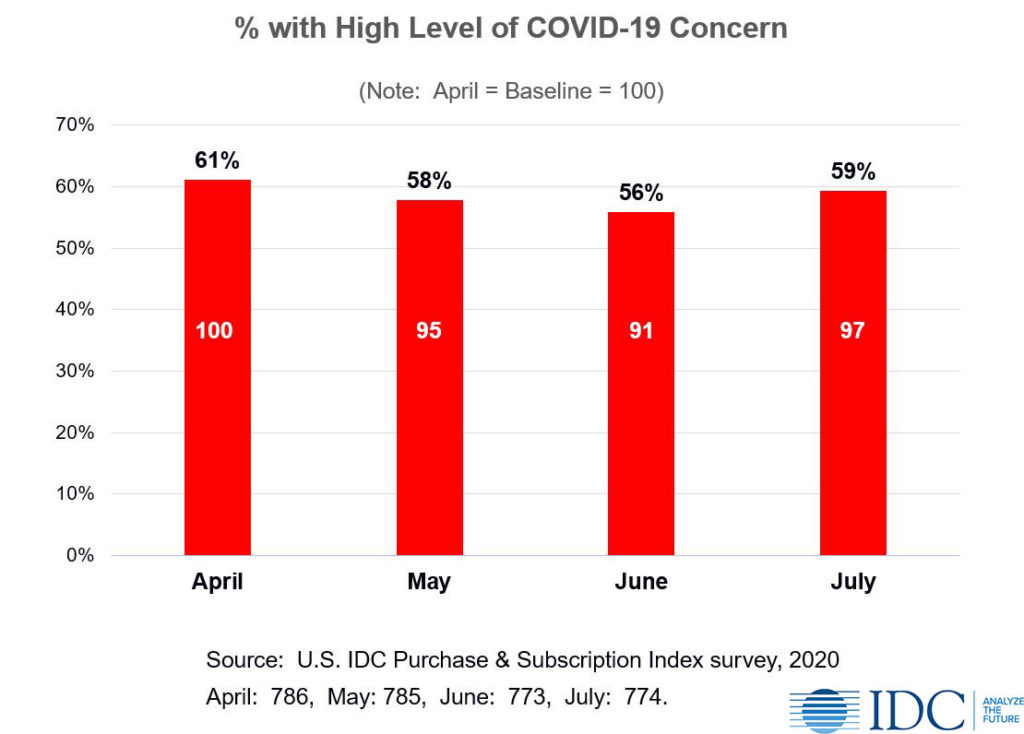

After trending down for two months, concern about COVID-19 has jumped up again, as the number of cases grows across the country.

Key Takeaways & Action Items for Consumer Marketers

- Self-reported consumer tech spending remained strong in July, bolstered by strong device spending with PCs and Tablets, smart home devices, gaming devices and accessories, and phone accessories all items of strong interest.

- Use these devices to drive traffic online or in-person.

- Consumers’ appetite for more has softened somewhat as COVID concern has returned to near April levels, but there is still even more potential among those with higher incomes.

- Prudent, high income consumers need reinforcement to follow through on their desires and plans.

- For devices, emphasize value and the “smartness” of purchasing right now and doing so will help others and the country by providing jobs and income.

- On the services side of the equation, consumers continue to rely on bundling as a strategy to drive better value for the money.

- Create awareness of your options for bundled services.

- Prudent, high income consumers need reinforcement to follow through on their desires and plans.

- Lower income consumers can never be counted out, as demonstrated by their strong device spend in July.

- Sales promotions and bundling initiatives can help to sustain this.

- Make sure that consumers have a payment alternative which fits their budget and reality.

- Be prepared for the next wave.

- While things may stabilize over the next month, high levels of disposable income and another round of stimulus are likely to help reinforce spending.

IDC’s Consumer Technology Strategy Service (CTSS) leverages a system of frequent consumer surveys to provide B2C marketers with the full view of the consumer they need to anticipate and meet changing consumer needs and to outperform their competitors. This includes robust monthly data, timely insights, quarterly webinars, and ongoing analyst access.

In addition to my syndicated service, I work closely with client on custom research projects and consulting. Learn more about our CTSS research and services: