Blockchain, while still a nascent space, continues to mature. While the global blockchain and distributed ledger market evolved slowly, specific use cases for the technology have moved forward steadily. The initial excitement about blockchain across nearly every sector and industry has given way to a realistic appraisal of the technology and an emphasis on business value.

While the impact of COVID-19 has affected enterprise spend on blockchain, but it has also emphasized the fragility and vulnerabilities of areas such as global supply chains, food supplies, oil and gas production, and financial services. Thus, the effects on enterprise spend on blockchain are smaller than other emerging technologies. The IDC Worldwide Blockchain Spending Guide still expects a 5-year compound annual growth rate (CAGR) of 46.4% in the coming 5-year period.

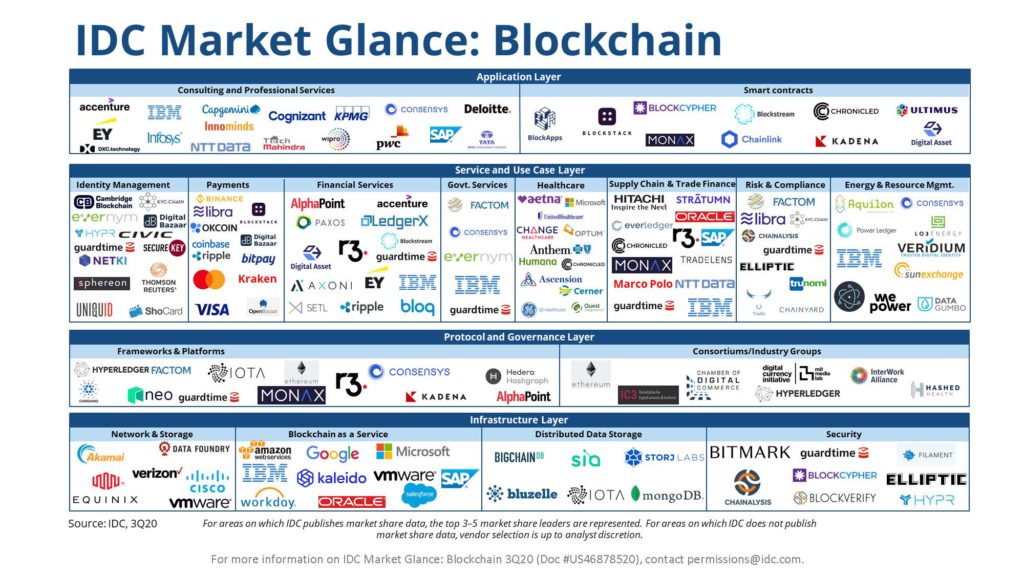

As blockchain has developed as a product, the protocols, governance models, and platforms have also matured, providing developers, line of business owners, and technology leaders with more robust, capable and useful tools for enterprise applications. There are still areas where development of core technical issues are necessary, especially in smart contracts and oversight in heavily-regulated industries, but the focus is moving away from how the technology works and towards where it can be applied.

However, there are still challenges that continue to fuel skepticism and hinder the adoption of blockchain and distributed ledgers. Those challenges are due in large part to the fact that distributed systems require a different approach to legacy technology. That approach often entails vendors, partners, and industries working in coordination. That remains a difficult issue to overcome and introduces concerns over risk, and compliance.

The slow maturation of blockchain has caused many vendors who initially offered blockchain services and products to de-emphasize their blockchain solutions. This is especially true at the infrastructure layer—the base of the technology stack— where storage and networking providers have had a difficult time finding a compelling message. The “Blockchain Stack” model itself has begun to change, with players across the stack approach different use cases, markets, and applications as opportunities present themselves. The result is a market that is still in flux as vendors figure out their business models:

Learn more about IDC’s blockchain outlook, and read the complete Market Glance document: