It’s no secret that enterprise workloads continue to move, migrate, and modernize with the help of cloud infrastructure. Cloud infrastructure services have become a foundational part of the enterprise IT landscape and will act as the growth engine for the enterprise infrastructure market for the foreseeable future.

But how does this market break down by workload type? That is the question we have been asking and discussing with clients over the past several years. These discussions, along with additional research and modeling have led us to produce IDC’s first workloads-based segmentation of the combined cloud IaaS and PaaS markets. Three thematic highlights from the research include:

- Enterprises are using cloud infrastructure to help scale and modernize – regardless of workload type. At the highest level, enterprises say their top priorities with cloud infrastructure include scaling existing applications using cloud resources; and modernize applications already in the cloud using cloud-native services (e.g., containers, PaaS, serverless). In large part, the continued pace of enterprise data growth is driving this trend. Enterprises are constantly seeking ways to manage data efficiently and cost-effectively – this applies to all workloads.

The second key factor is making this data accessible to adjacent services (e.g., analytics, compliance, databases). Increasingly, this access can be done natively in the cloud within a single ecosystem. - It’s impossible to generalize which workloads are “fit” or “unfit” for cloud. Recent survey data indicates 60% of enterprises have migrated workloads out of the public cloud. But the reasons for doing so vary, as do the workload types. Years of cloud migration research by IDC indicates many workloads will fluctuate between deployment locations until they reach an optimal balance of cost, performance, and security. Achieving this balance is more important to most enterprises than the location itself, which is why so many have adopted hybrid cloud and multi-cloud deployments to diversify their infrastructure options.

- Cloud infrastructure services are highly COVID-proof. Cloud infrastructure will remain an essential part of enterprise recovery strategy as IT organizations reevaluate budgets, build infrastructure focused on business resilience, and work toward operating efficiently and managing risk in a post-COVID-19 world. This bodes well for the long-term performance of the market and its impact on all workload types, as 80% of enterprises we surveyed said their cloud IaaS budget will stay the same or increase, regardless of the pandemic.

By the Numbers: Top Workloads Run on Public Cloud IaaS and PaaS by Revenue

Looking at the numbers provides some important context to these themes:

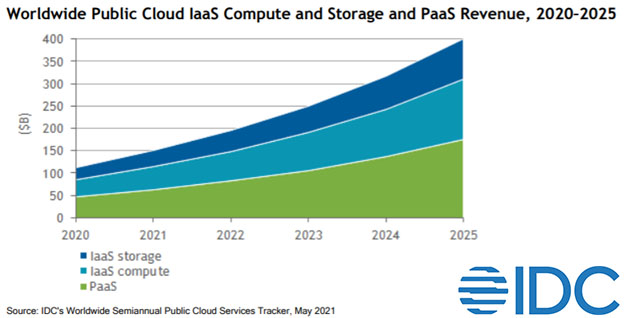

The combined Public Cloud IaaS and PaaS market is forecast to grow to $400 billion in 2025 with a compound annual growth rate (CAGR) of 28.8% during the 2021-2025 forecast period. This total market size of $400 billion is then broken down by workload type. Highlights include:

Workload Highlights by Revenue Share:

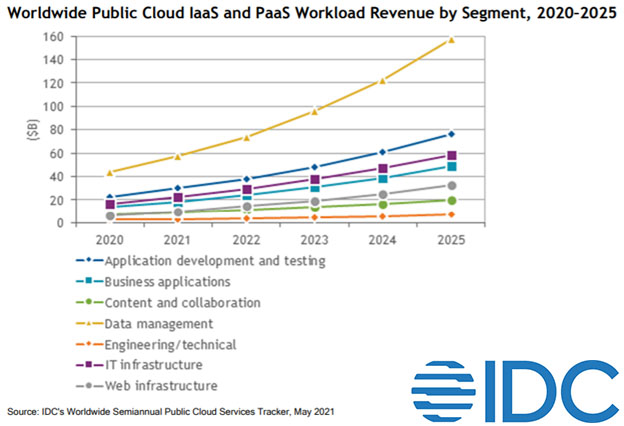

- Overall, Data management and Application development and testing are the largest workload segments, comprising 39% and 20% of the total market respectively. These are the primary workloads supported by PaaS solutions and thus benefit from a significant portion of revenue in that segment.

- When we look at just IaaS revenue, IT infrastructure workloads comprise the majority of share at 25%, followed by Business applications at 21%, and Data management at 20%.

Workload Highlights by Revenue Growth:

- Overall, Unstructured data analytics/data management and Media streaming are forecast to be the fastest growing segments, with CAGRs of 41.9% and 41.2%, respectively.

- Other business applications, file and print, and content applications will grow slower than the overall market average — but still in the double digits throughout the forecast period — at CAGRs of 15.5%, 19.5%, and 19.8%, respectively.

What is an Enterprise “Workload” and Why Did IDC Produce This Forecast View?

IDC has produced Workloads Trackers for the enterprise storage systems and server markets for years. These Trackers count server and storage system configuration, deployment, and ultimately revenue associated with running specific enterprise IT workloads. IDC’s Workloads Taxonomy classifies these workloads into seven categories and 18 types. Examples include Application Development, Business Applications (e.g., CRM, ERM), Data Management (structured and unstructured workloads), and Web Infrastructure (media streaming, web serving).

IDC’s IaaS and PaaS Workloads forecast builds on this foundational taxonomy and extends the market view from traditional servers and storage systems to now include the revenues associated with public cloud infrastructure services. This addition helps complete IDC’s comprehensive view of revenue to support workloads across all infrastructure types, whether that means dedicated infrastructure, private cloud, or public cloud.

Conclusion: Living with Workload Ambiguity

When it comes to enterprise workloads in the cloud, we continue to reiterate the belief that workload migration is a journey, not a destination. Each individual enterprise, IT buyer, business unit, application owner, and application developer potentially has input into which workloads will benefit the most from a particular deployment type, and whether or not they need to migrate to/from the cloud.

IDC research shows that there isn’t a simple way of categorizing workloads as “suited for the cloud” or “not suited for the cloud” based on the workload functionality, and functionality alone is not a sufficiently strong criteria to prioritize workloads for movement. Within every workload, as defined by IDC, applications and specific customer installations of an application can fall anywhere along a spectrum of least to most suited for migration, based on various factors, some of which have little to do with the workload itself.

Complicating matters further is the fact that not every workload is an island. Although we separate workloads into discrete categories for the purposes of our analysis, the reality is that many use cases require multiple workloads operating together, often in close proximity, to deliver the desired user experience.

Given this ambiguity, IDC will continue to improve its infrastructure workloads research in an attempt to deliver actionable information to both IT providers and buyers. We’ve begun producing detailed analysis of specific workload segments, which brings together all of IDC’s workloads research including both market and survey data. Explore our latest Market Presentation here: