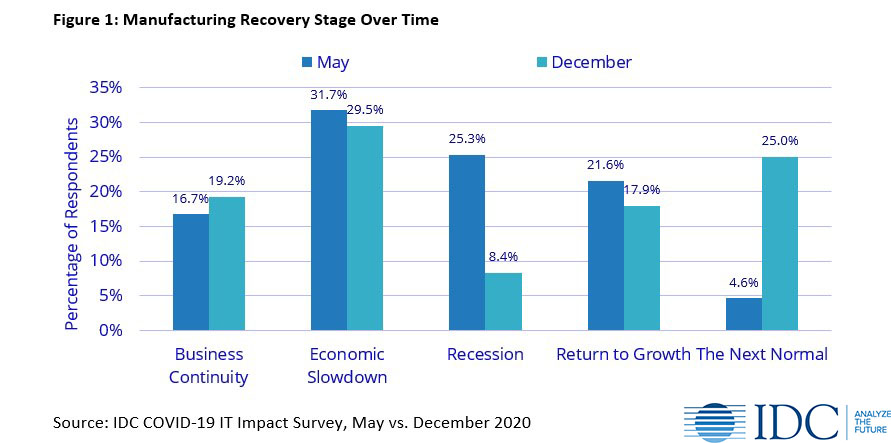

The disruption caused by COVID-19 will have a long-lasting impact on all industries, but in my opinion, manufacturers have had to adapt the most. In fact, IDC’s Worldwide ICT Spending Guide has shown that roughly $1.3 Trillion has been lost because of COVID-19, with the manufacturing industry bearing the greatest portion of this loss. Manufacturers continue to struggle with supply chain disruption, evolving government/regulatory requirements, and shifting production capabilities to meet public demand for their goods and services. The manufacturing recovery process is still on-going when looking at some of IDC’s recent COVID impact studies. When comparing May to December there are two key points here that I wanted to hit on (Figure 1). First, roughly the same percentage of manufacturers are still in phase 1/2 where keeping the doors open and dealing with slowdowns in business are the top priority. Second, there is a clear shift where a portion of the industry have progressed from phase 3 into phase 5.

The reason this is important is because it points to the larger theme that we have been seeing across the industry – there were manufacturers that were better prepared to respond to disruption. The common denominator among these successful companies, they had made investment prior and throughout COVID in digital technology. There is a ‘digital divide’ that has formed between these two types of companies, with digitally enabled manufacturers feeling less of an impact and further along in their recovery efforts. These manufacturers are now focused on innovating and trying to capture market share, while non-digital manufacturers are still focused on cost cutting and selling off high-risk projects.

The rapid pace of change has led the industry to start defining their future success by how well they can react to market disruptions – which IDC calls operational resiliency. Customer and market expectations for more personalized products, deliveries, and services are driving change and creating opportunities for a company to transform how its operation stays aligned with its markets. The disruption caused by COVID has served as a wakeup call for most in the industry to realize that change needs to occur, with less than 20% of manufacturers believing their business model is future proof.

As we enter 2021, manufacturers will need to continue to think of services as a key driver for differentiation and not an aftersales activity required because of a product sale. This mindset shift will require service specific investments and digital initiatives that connect service history and customer data with other enterprise applications. High Tech manufacturing is a segment that perfectly highlights the commoditization that has occurred and the shift into software to drive differentiation. Evolving from an equipment manufacturer business model into a software company is typically a multi-phase process which begins with integrating solution-specific software alongside the current solution-specific hardware and then offering added value software packages in addition to the traditional hardware-based offering. To accelerate this shift into software services a practice that is often employed by organizations is merger and acquisition (M&A) activity.

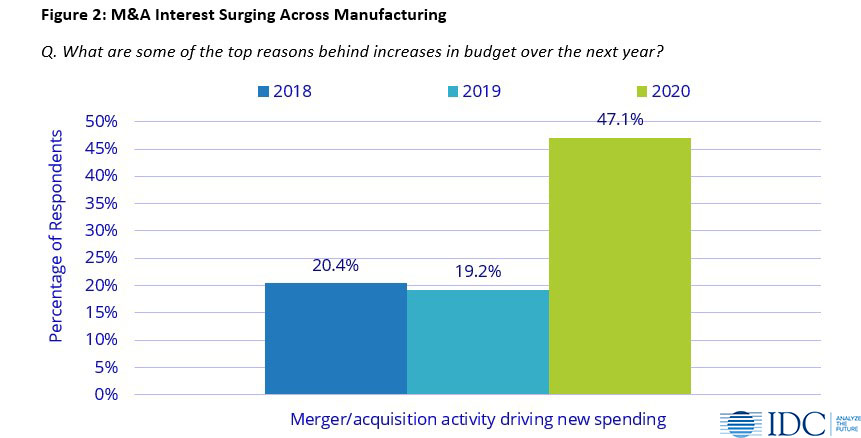

The increased focus on M&A activity is an interesting one when comparing to past years, with roughly 20% of manufacturers surveyed saying M&A activity is one of the top reasons behind budget increases (Figure 2). However, when we look at the results for 2020 and into 2021 there is a sharp jump in interest across the industry. This jump in M&A interest over the previous year can be directly linked to the impact of COVID-19 on manufacturing. Even more so when breaking down the numbers by process and discrete manufacturing. Process manufacturing still has doubled with 41% of the industry saying M&A activity will be high, discrete manufacturing (which was much harder hit by COVID) had 54% of respondents focused on M&A activity.

While we expect to see manufacturing spend increase in 2021 across the board, thinking back to manufacturing’s recovery progress, there are companies better positioned to take advantage now. It will be those digitally enabled companies that will lead the charge in making targeted investments, using M&A to further their transformation efforts. While those non-digital manufacturers that are still struggling will continue to fall further behind.

Disruption brings challenges but also opportunity. Manufacturers that are focused on resiliency and using data to make decisions will be best positioned to succeed. The digital divide has only widened because of COVID-19, this has resulted in many forward-thinking manufacturers to explore potential M&A activity that can accelerate their transformation journey. There will be many undervalued assets available for companies that are able to spend. As manufacturers continue to look for ways to expand into new markets and get closer to customers, the shift to offering products and services will be key. There are challenges that need to be considered when integrating new acquisitions into the business but being in the position to acquire is the first step.

For additional research related to manufacturing priorities over the next year split by different value chains and sub-segments please refer to IDC’s value chain investment guides:

https://bit.ly/3mzAqlwIf there is one key lesson to take away from the past year, it’s that being proactive rather than reactive will lead to success in today’s rapidly changing environment. The future of the Manufacturing Industry is dependent on the digital transformation that is already in motion for many organizations; the convergence of IT and OT. These innovations are changing the Manufacturing Industry as we know it; creating what we like to call, Industry 4.0. In order to adopt Industry 4.0 strategies, you’ll need to follow five crucial steps. To learn more, read the eBook, Five Steps to Industry 4.0 in Manufacturing. Click the button below to download.