This blog complements a recently published thought leadership paper (download for free) as well as an IDC Webinar on 25 February 2021 (register for free).

The Rise of ESG

The character of corporate sustainability has been changing significantly over the last few years. The topic has become much more than a normatively driven way for businesses to do good. Many enterprises are in the process of moving from a simple corporate social responsibility (CSR) approach to a more integrated, purpose-driven and metrics-focused concept of looking at sustainability strategically in the context of improving operational and financial performance, risk profiles, employee attraction and retention, brand value, etc. Business strategies focusing on environmental, social, and governance (ESG) topics account for that shift by addressing sustainability in a more holistic manner.

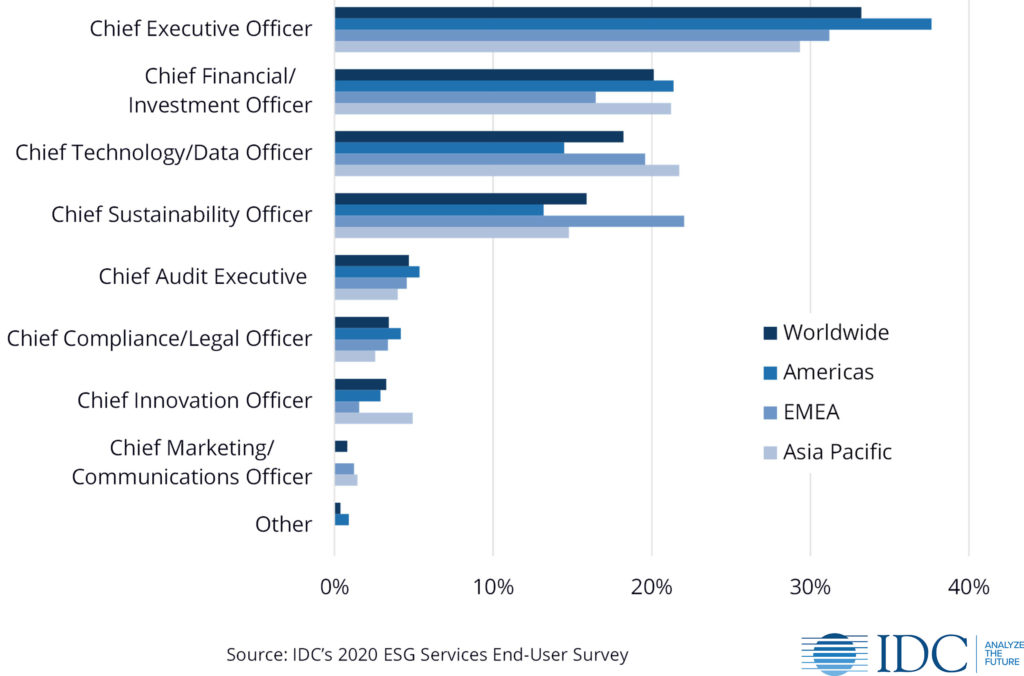

IDC’s research shows that sustainability/ESG has become primarily a CEO/CFO-level topic. This certainly constitutes a change compared to previous views on corporate sustainability and highlights the level of coordination that is necessary amongst members of the c-suite and board to ensure the adoption of a successful sustainable business strategy.

“Who is mainly responsible for the sustainability/ESG strategy and implementation in your organization?”

CSR, ESG, and Purpose

For a long time, the principal purpose of corporations was defined as maximizing shareholder return, e.g., expressed by Milton Friedman’s famous characterization of corporate social responsibility as “hypocritical window-dressing” in an article he wrote in 1970 for The New York Times Magazine. Today, companies are looking at sustainability in different ways – commercially and non-commercially focused:

- Commercially through metrics driven ESG efforts that are part of a sustainable business strategy

- Non-commercially through normatively driven corporate social responsibility (CSR) and philanthropical efforts

A purpose-driven strategy aligns an organization’s normative goals and efforts with its need for positive operational and financial performance, and risk management. This requires companies to adhere to ESG reporting standards and frameworks and use ESG metrics to capture, assess, report and benchmark relevant sustainability information.

While companies are increasingly aligning their sustainability efforts with their stated purpose, there is still a large prevalence of boilerplate language being used in reporting and disclosing these efforts, which makes it difficult to hold enterprises accountable. This is particularly relevant in times when companies around the globe are putting out bold statements about their environmental and social responsibility: accountability and putting words into action are a central element of completing the switch from CSR to truly impactful sustainable business strategies.

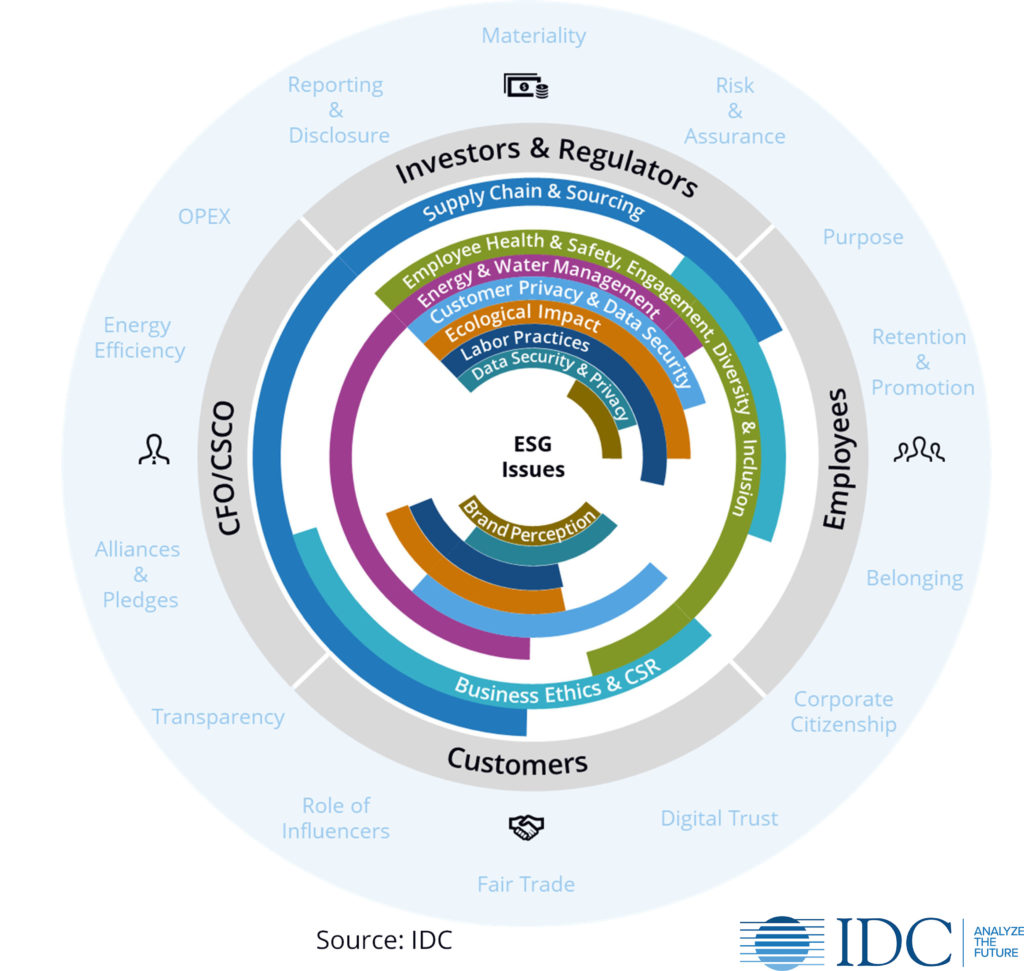

Corporate ESG Stakeholder Groups, Topics, and Issues

Intangibles such as intellectual capital, customer relationships, and companies’ brand value vis-à-vis its employees and customers are increasingly affecting valuations, creating additional pressure for companies to find appropriate ESG metrics for the sustainability topics that matter to their business. The handling of ESG issues (greenhouse gas emissions, water usage, diversity and inclusion, human rights, etc.) can affect business performance in different ways, e.g., revenue growth (demand for products and services), cost (operational efficiency), assets and liabilities (valuation), or cost of capital (operational risks).

While there have been various efforts to standardize and consolidate ESG reporting standards and frameworks, ratings, etc., we observe a continued struggle on the end-user side to prioritize the demands and requirements that companies receive from different stakeholders and the resources they are able to deploy to respond to these demands. However, it will be critical for companies to find effective ways of capturing, reporting and disclosing, assessing, and benchmarking their ESG performance using relevant and standardized metrics, in order to fully capture the opportunities that lie within ESG and to underline their commitment to their stated purpose.

The Growing Landscape of Stakeholder Groups That Increases the Complexity of ESG Measures

Corporate value is no longer defined by the creation of shareholder value only. To determine material and other important sustainability topics, companies also need to take into consideration a diverse set of stakeholders that affect and are affected by an organization’s business. While investors remain an important and influential stakeholder group, other stakeholder groups such as employees and customers need to be taken into consideration when companies define their purpose and strategy.

When it comes to ESG issues, they oftentimes affect different stakeholder groups- but they don’t always do or they might affect stakeholder groups in different ways, creating different kinds of demands and requirements. Stakeholders can be external (investors, customers, etc.) or internal ones (CSCO, employees, etc.) or sit somewhere in between (suppliers, communities, etc.). Identifying material and relevant ESG topics in the context of all stakeholder groups is essential for fully leveraging ESG as a driver for business performance and a hedge against sustainability-related business risks.

This also means that companies might need to blend CSR- and ESG-focused approaches and allocate resources accordingly. For instance, investors are mostly interested in enterprises’ performance on material ESG issues and sustainability topics that can potentially become financially material. This evaluation is highly industry-specific and focused on topics that really affect the enterprise value of a given company. Employees and customers, on the other hand, do not necessarily care about ESG materiality but about topics that they consider important- regardless of industry or impact on a company’s core business. This requires additional efforts that are more focused on brand value and reputational risk, purpose, belonging, etc., and are not always aligned with topics that are considered material.

Conclusion

The complexity and multi-faceted character of sustainability requires companies to take a comprehensive, end-to-end approach that considers various aspects of sustainability, e.g., geographical and industry-specific differences, normative and business-driven implications, internal and external stakeholders, and its impact on the different business functions. In many ways, sustainability has become a new business imperative, similar to “digital”. It will be ingrained into everything that businesses do and can and should not be seen as a separate or “nice-to-have” item any longer.

If you would like to learn more about IDC’s ESG Business Services research, visit our website or watch this brief video.

Learn more about making the business case for sustainability with our webinar on February 25 at 11am EST. Register now to reserve your space: